“That, given the choice between doing what is right and doing what is not right,

[…] government will take the latter course every time.”

Tom Wilkinson

Introduction

For over a decade, caregivers at Positive Outcomes, Inc., a New Mexico-based company providing physical therapy, early childcare, and personal care services, were subjected to a predatory lending scheme orchestrated by former state representative Tara Jaramillo. Positive Outcomes, which serves vulnerable communities with services ranging from developmental therapies to family advocacy, allegedly engaged in payday advance lending without a lending license from the New Mexico Regulation and Licensing Department, targeting its employees with loans carrying a bi-weekly interest rate of 15%. Under these terms, a two-day loan saw the equivalent annual interest rates as high as 2,737%.

The scheme disproportionately affected low-income and Native American caregivers, who were already economically vulnerable. These employees found themselves trapped in cycles of debt as repayments were deducted directly from their wages, leaving many without adequate take-home pay. Whistleblower Noah Jaramillo, a former employee and relative of Tara Jaramillo, stepped forward with evidence of these predatory practices and alleged misuse of Medicaid funds. Despite his detailed complaints to the New Mexico Department of Workforce Solutions, the Human Services Department, and the Attorney General’s Office, systemic inaction allowed the practices to persist.

Governor Michelle Lujan Grisham, who received over $3,600 in campaign contributions from Tara Jaramillo, should be scrutinized. Her administration’s agencies failed to act decisively despite mounting evidence. Current Attorney General Raúl Torrez has yet to thoroughly investigate these allegations, raising questions about whether political connections have shielded Jaramillo from accountability.

Systemic failures allowed Positive Outcomes to exploit the caregivers entrusted with improving the lives of vulnerable community members. These workers were financially ruined by the organization that claimed to empower them, and the state agencies tasked with protecting them turned a blind eye.

The Black Market

Government price fixing created the perfect environment for predatory practices to flourish. The exploitation of financially vulnerable employees at Positive Outcomes, Inc. did not occur in a vacuum. Their dependence on illegal payday loans from their employer was not merely a result of Tara Jaramillo’s willingness to break the law, it was also a predictable consequence of overregulation in New Mexico’s financial sector.

Previous investigations into financial inclusivity and credit access like No Loan for You! and No Loan for You, Too! exposed the consequences of state-imposed interest rate caps, which have severely limited access to legal, regulated financial alternatives for low-income borrowers. In reality, the policies designed to “protect” consumers from predatory lending have driven desperate borrowers into the arms of loan sharks operating outside the legal system.

Price Fixing

Historically, small-dollar credit providers have filled a crucial financial gap for individuals who are unable to qualify for traditional bank loans. These specialized short-term loans provided quick access to cash for emergency expenses, utility bills, or unexpected medical costs.

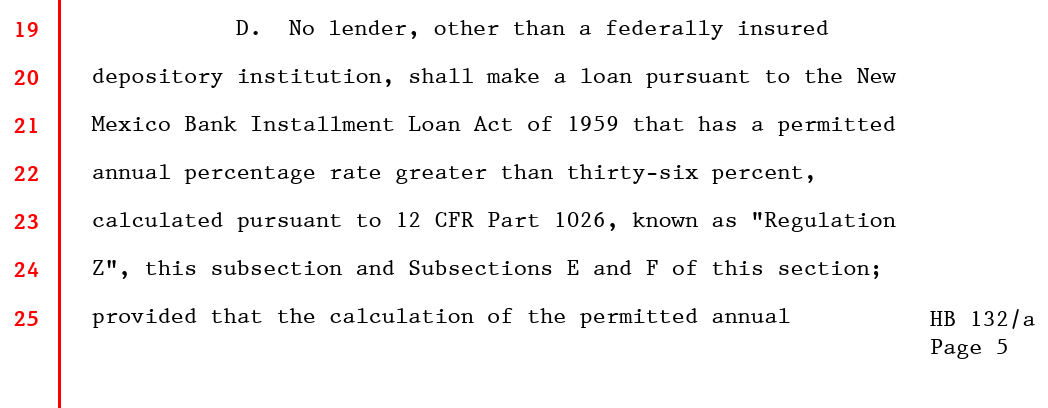

However, New Mexico’s HB 132 (2022) imposed a 36% APR cap on small loans, effectively banning short-term lending and eliminating a large segment of legal, regulated financial services that many working-class and underbanked New Mexicans relied on.

Three themes stood out: (1) Due to hidden eligibility requirements, the “consumer-friendly” small-dollar loans offered by big banks are largely inaccessible, especially to unbanked or underbanked populations; (2) Credit unions, often promoted as an alternative, rarely offer viable short-term loan options, particularly to non-members or those with limited credit histories; (3) Many borrowers, particularly those living paycheck to paycheck, have no viable legal borrowing alternatives when faced with financial emergencies.

This regulatory squeeze did not eliminate demand for short-term loans; it simply eliminated legitimate supply. In doing so, policymakers created a vacuum, which unregulated and illegal lenders, like Jaramillo’s scheme, stepped in to fill. By capping rates at 36%, the state made it financially unsustainable for licensed lenders to offer high-risk loans, effectively outlawing the only viable products for many low-income borrowers, ushering in an unlicensed, unregulated, and unaccountable loan-shark operation.

Take the Blinders Off

The lack of access to legal credit options left Positive Outcomes employees with no alternatives when they needed money quickly. For workers earning modest wages and struggling to cover unexpected expenses, the promise of a payday advance from their employer, no matter how exploitative, was better than nothing.

Jaramillo weaponized this reality, knowing her employees could not go to a regulated lender. Unlike legal small-dollar lenders, who must disclose fees and adhere to lending laws, Jaramillo was able to:

- Issue loans without licensing or oversight.

- Charge unlawful interest rates (over 2,700% APR) without consequence.

- Use wage garnishment to guarantee repayment, trapping employees in a cycle of debt.

Despite enforcing lending laws against licensed lenders, state agencies failed to regulate or even acknowledge the existence of an emerging black market for small-dollar loans. With the government unwilling or unable to police illicit lending, Positive Outcomes’ payday advance scheme flourished in the shadows, harming the people the government claimed to protect.

“Protection” Leads to Exclusion…

Low-income workers and the unbanked do not simply stop needing loans because the government restricts them. Instead, they turn to:

- High-fee overdrafts or rent-to-own agreements.

- Unlicensed “loanshark” lenders operating outside legal oversight.

- Employers who abuse financial desperation, as seen at Positive Outcomes.

Jaramillo’s ability to exploit her workers was both an ethical failure and an economic inevitability in a state where misguided regulations had stifled financial competition.

The regulatory war on payday lending did not reduce financial hardship; it simply made financial desperation more profitable for bad actors. Instead of ensuring fair access to credit, policymakers have forced the most vulnerable borrowers into situations where they have no choice but to accept illegal, abusive terms.

…Exclusion Leads to Exploitation…

Former and current employees of Positive Outcomes, Inc., a company owned by former State Representative Tara Jaramillo, have come forward with allegations that the business has been engaging in illegal payday lending practices without a license. The company, which provides in-home caregiving services, has reportedly issued short-term, high-interest loans to employees, deducted payments directly from their wages, and charged rates that far exceed legal limits.

Beyond the legal concerns, these loans primarily targeted financially vulnerable workers, many of whom are Native American caregivers. Despite the severity of these allegations, state regulatory agencies have failed to take action, prompting concerns about political influence and the enforcement of consumer protection laws.

The Evidence

Evidence provided by whistleblowers and former employees suggests that Jaramillo issued payday loans without proper licensing and charged employees an interest rate of over 2,700% APR, far above the legal cap of 36% set by HB 132 (2022).

The Regulation and Licensing Department does not list Positive Outcomes on its list of liscensed lenders.

Key allegations include:

- Operating Without a License: The New Mexico Small Loan Act of 1955 requires that any entity issuing loans of $10,000 or less be licensed by the Financial Institutions Division (FID). However, as of December 31, 2024, neither Jaramillo nor Positive Outcomes is listed as a licensed lender in New Mexico’s small loan directory.

- Excessive and Illegal Interest Rates: Employees reported being charged 15% interest biweekly, translating to an annual percentage rate (APR) between 390% and 2,700% depending on the timing and repayment of the loan, well in excess of the state’s legal limit.

- Wage Garnishment Without Disclosure: Borrowers were required to sign agreements allowing loan repayments to be deducted from their paychecks. However, they were reportedly never provided with documentation of loan terms, including the total cost of borrowing, which violates the Federal Truth in Lending Act (TILA).

- Potential Medicaid Misuse: A whistleblower alleged that funds used for these loans may have originated from advance Medicaid payments to Positive Outcomes, a claim that could carry significant legal ramifications.

These lending practices have amounted to a predatory loan scheme that trapped victims in cycles of debt. Unlike regulated lenders, who must comply with transparency and consumer protection requirements, Jaramillo’s operation functioned outside legal oversight.

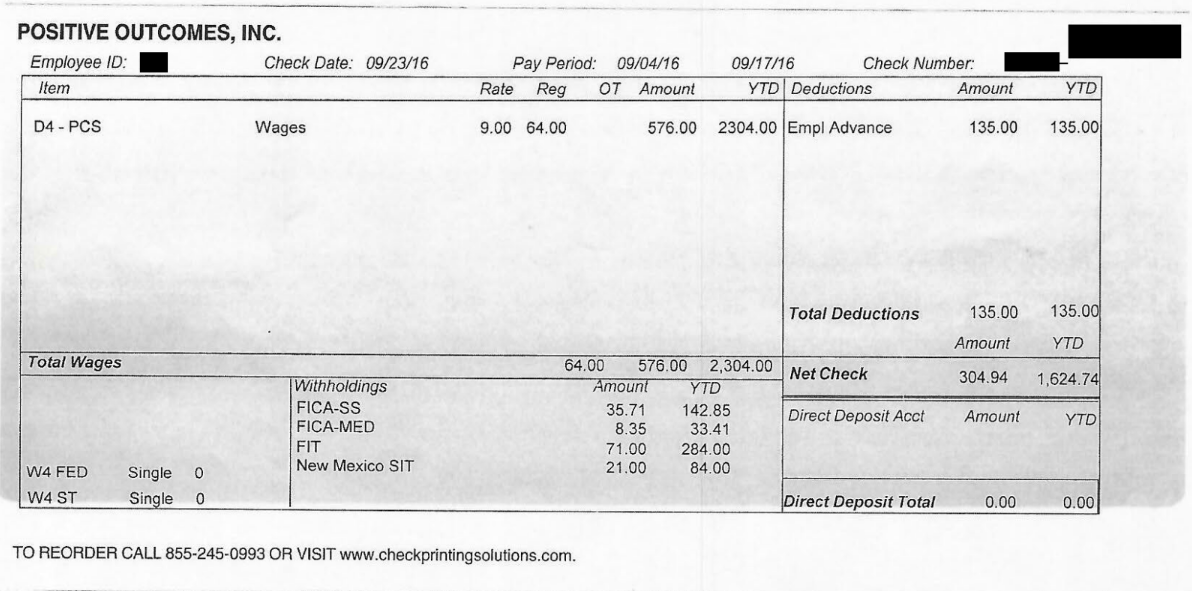

As part of its now-stalled investigation into Positive Outcomes, the New Mexico Department of Workforce Solutions (DWS) subpoenaed a series of documents, including pay stubs, internal correspondence, and loan repayment schedules, demonstrating the scope and structure of the unlawful lending practices.

Just Politics

Despite the clear violations of state and federal lending laws, complaints filed with multiple agencies, including the New Mexico Attorney General’s Office, the Human Services Department, and the Department of Workforce Solutions (DWS), have resulted in no enforcement action.

- A detailed complaint filed with the Attorney General’s Office was reportedly passed off or ignored, despite evidence of unlawful lending.

- The Department of Workforce Solutions (DWS) launched an investigation in February 2024 but suddenly stalled in July, with no explanation provided to whistleblowers.

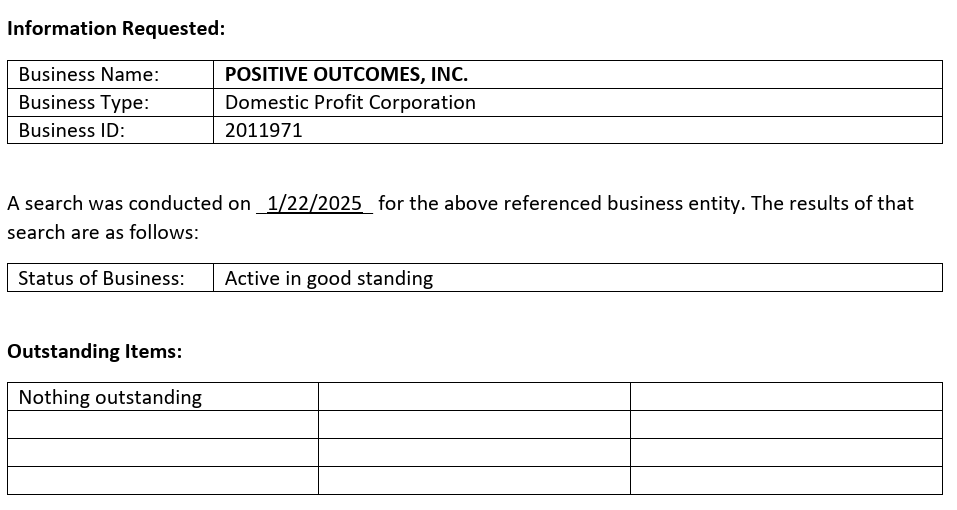

- A Business Audit Request for Positive Outcomes, released by Secretary of State Maggie Toulouse Oliver in 2025, showed no indication of illegal lending practices, despite extensive documentation from former employees.

Jaramillo has made campaign donations to key state officials, including Governor Michelle Lujan Grisham, Attorney General Raul Torrez, and Secretary of State Maggie Toulouse Oliver. These contributions raise questions about whether political influence has affected the apparent lack of enforcement.

Additionally, while New Mexico’s Regulation and Licensing Department (RLD) publicly lists enforcement actions for other industries, such as the Cannabis Control Division and the Securities Division, no such transparency exists for financial institutions, making it unclear whether any action has been taken against Positive Outcomes.

What Should Have Happened?

Under HB 132 (2022) and existing lending laws, businesses issuing short-term, small-dollar loans are required to:

- Obtain a state lending license before issuing loans.

- Disclose the full loan terms to borrowers, including APR and total repayment cost.

- Cap interest rates at 36% APR for consumer loans.

- Avoid wage garnishment without proper legal procedures.

Jaramillo’s alleged actions violate these protections, yet enforcement agencies have failed to intervene.

FID is responsible for enforcing lending regulations but only has authority over licensed lenders. Because Positive Outcomes was never registered, the agency may lack jurisdiction to penalize Jaramillo, which might constitute a loophole in consumer protection enforcement.

The allegations against Positive Outcomes, Inc. paint a troubling picture of unlicensed lending, predatory lending practices, and abusive wage garnishment that left financially vulnerable employees in a cycle of debt. Despite clear violations of lending laws, regulatory agencies have failed to take action, raising questions about the influence of politics and the ability of state agencies to protect consumers from predatory financial schemes.

As public scrutiny grows, New Mexico’s leadership faces a critical choice: Will they uphold consumer protection laws or allow politically connected businesses to operate outside the law?

For the employees affected, the question is even more urgent: What recourse is available when a company operates beyond the reach of state regulators?

The answers remain to be seen.